Introduction

When the United States and Israel launched a combined Operation Epic Fury on Iran on 28 February, it was widely anticipated that Iran would weaponize the Strait of Hormuz as leverage in the conflict. However, the scale of economic disruption generated through the closure and militarization of the waterway appears to have exceeded even Iranian expectations. The crisis was further intensified by the reported US naval blockade targeting Iranian ports, effectively creating a dual disruption across both outbound Gulf energy flows and Iranian maritime access.

The resulting disruption to maritime traffic and energy exports has severely affected global trade markets and renewed concerns regarding the vulnerability of strategic chokepoints within the contemporary international system. The IMF projects that global economic growth could slow to around 2 percent next year if energy supplies fail to normalize, a scenario that now appears increasingly plausible. For context, the global economy has grown by less than 2 percent only four times since 1980.

The current Hormuz crisis, therefore, demonstrates not only the economic vulnerability of the global trading system but also the growing feasibility of weaponising international waterways for geopolitical leverage.

Strategic Importance of the Strait of Hormuz

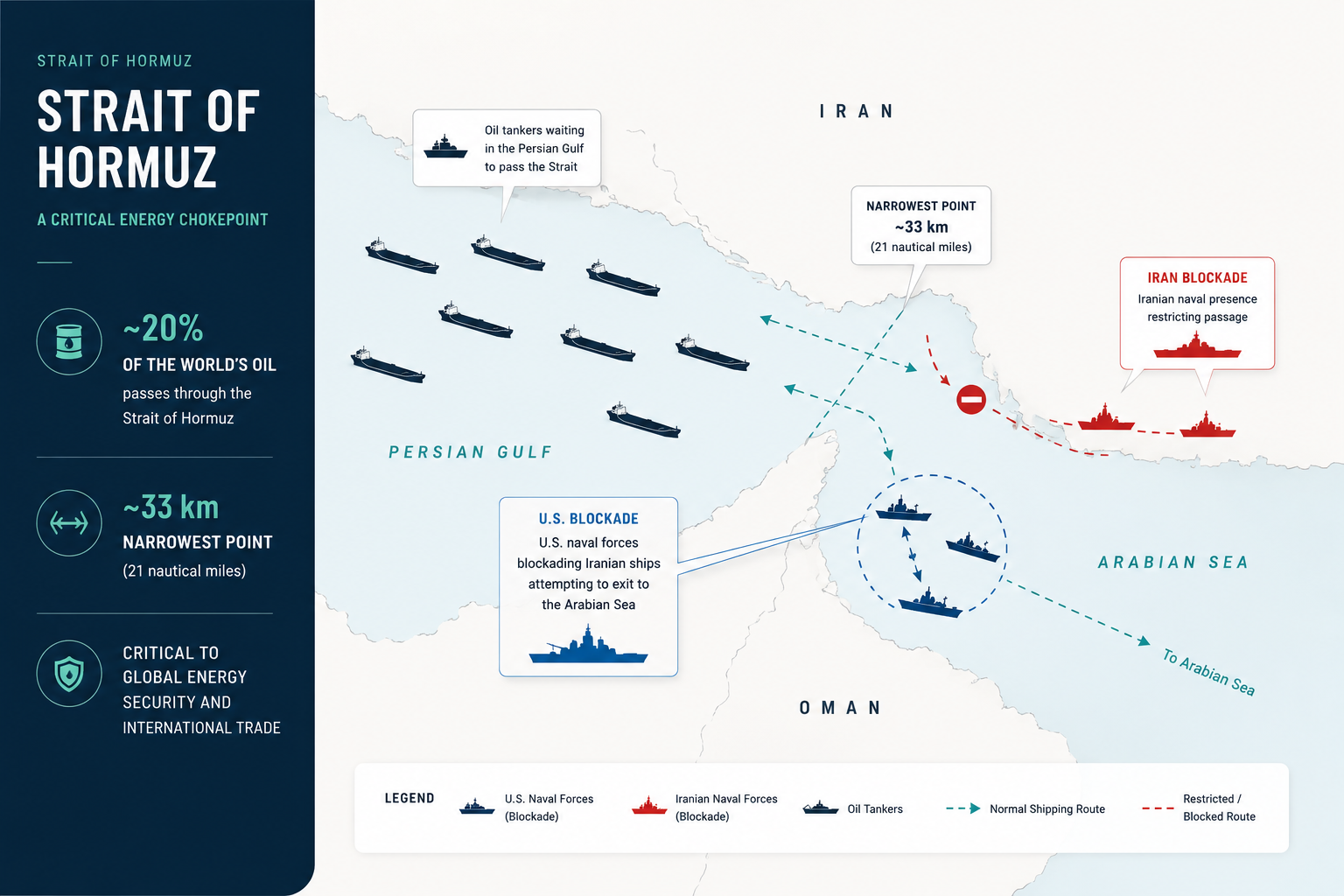

The Strait of Hormuz remains one of the most strategically important maritime chokepoints in the world, connecting the Persian Gulf with the Gulf of Oman and the broader Arabian Sea. At its narrowest point, the strait is only around 21 miles (33 km) wide, yet it facilitates nearly 20 percent of global energy trade.

Beyond crude oil, the strait also serves as a major transit route for critical commodities, including helium, fertilizers, petrochemicals, and other industrial materials essential for global manufacturing and supply chains. Consequently, even limited disruptions to maritime movement through the strait generate immediate and far-reaching consequences for international trade, food security, and energy markets.

Prior to 28 February, nearly 140 oil tankers reportedly transited the strait daily. However, following the escalation in conflict, tanker traffic reportedly dropped to fewer than 10 vessels per day, illustrating the scale of disruption imposed on global energy flows.

This infographic is AI-generated and intended for illustrative purposes only

Oil Market Shock and Global Economic Consequences

Of all the commodities transiting the Strait of Hormuz, energy exports remain the most strategically significant. The resulting supply disruptions and sharp rise in energy prices have been particularly visible in energy-import-dependent countries such as Pakistan and the Philippines, where governments introduced fuel-saving measures that directly affected day-to-day economic activity.

Major Asian economies remain heavily dependent on the Strait for their energy needs. Approximately 80–90 percent of Japan’s oil imports transit through Hormuz, while India depends on the strait for nearly 50–55 percent of its crude oil imports. China similarly relies on the waterway for an estimated 40–50 percent of its imported energy supplies. Disruptions to energy flows into these economies, particularly China, which remains a major global manufacturing hub, are increasingly contributing to shortages of important commodities across global markets, including Middle Eastern countries.

Moreover, oil occupies a unique position within the global economy because increases in oil prices do not remain confined to the energy sector alone. Rising oil costs increase transportation and export expenses, which subsequently contribute to inflation across broader markets. In response to inflationary pressures, central banks often raise interest rates, which in turn reduces commercial activity, weakens investment flows, and increases the likelihood of economic recession.

At the same time, the full economic impact of the crisis may not yet have materialized, as many oil tankers dispatched before the escalation continued reaching markets and several countries initially relied on emergency stockpiles. However, with the crisis approaching its fourth month, more severe supply disruptions may still lie ahead.

Additionally, replacing Gulf crude oil and gas would be extremely difficult, as alternative producers lack sufficient production capacity to offset the disruption of nearly 20 percent of global oil and gas flows. Consequently, a prolonged Hormuz disruption could become one of the most severe shocks to the global energy market.

Uneven Regional Impact

The consequences of the Hormuz crisis have not been distributed evenly across Gulf states.

Saudi Arabia and the United Arab Emirates have managed to reroute oil exports partially through alternative terminals in Yanbu and Fujairah, respectively, thereby bypassing the Strait of Hormuz. Kuwait, Bahrain, and Qatar, however, remain substantially more dependent on the strait and consequently face more severe economic disruptions and the prospect of economic contraction.

The crisis demonstrated that for many Gulf economies, the closure of Hormuz itself posed a greater threat than direct missile attacks from Iran. Given the heavy dependence of Gulf economies on crude oil and gas exports, disruptions in maritime energy transit rapidly translated into production losses, declining revenues, and broader economic instability.

IMF projections have reportedly reflected these pressures, with Kuwait’s real GDP projected to contract by 0.6 percent, Bahrain’s by 0.5 percent, and Qatar’s by a significantly steeper 8.6 percent.

This infographic is AI-generated and intended for illustrative purposes only

Weaponization of Waterways

One of the most significant lessons emerging from the crisis is that strategic waterways can now be effectively weaponized even by states possessing relatively weaker naval capabilities.

Iran demonstrated that it does not require complete naval superiority to disrupt one of the world’s most important maritime corridors. This signal is unlikely to be missed by other regional actors, including non-state organizations operating near critical chokepoints.

The crisis, therefore, establishes a dangerous precedent for the future. What the current Hormuz confrontation makes clear is that closing or threatening to close a strategic waterway has become operationally easier while the resulting economic consequences have become substantially more severe. Consequently, the crisis is likely to strengthen the incentives for governments and businesses reliant on critical sea lanes to diversify supply routes and invest in alternative transport and logistics infrastructure.

A comparable scenario could emerge in the Strait of Malacca in the event of a future China–Taiwan conflict involving the US. Under such circumstances, Washington may seek to leverage the strategic significance of the Malacca Strait to constrain China’s trade and energy supply chains. However, any disruption to maritime traffic through this critical chokepoint would also have significant unintended consequences for regional and global businesses operating across the Indo-Pacific, given the Strait’s central role in international commerce and supply-chain networks. Importantly, a waterway does not need to be fully closed to generate economic pain. Even the threat of disruption can sharply increase insurance premiums, force rerouting of shipping lanes, and destabilize commodity markets.

International Law and Strategic Transit

The US and Israeli strikes on Iran, along with subsequent threats by US President Donald Trump to blockade the Strait of Hormuz, indicate a growing willingness among major powers to impose extensive economic costs despite the broader implications for international trade and maritime law.

Previously, it might have been assumed that Washington would avoid actions capable of significantly disrupting passage through Hormuz due to the severe global economic consequences. The current crisis, however, suggests that such considerations now carry less strategic restraint.

Thus, the crisis raises broader concerns regarding the weakening of international norms governing transit through strategic waterways.

Regional Strategic Implications

The ongoing peace talks between the US and Iran, with the mediation efforts by Pakistan, may reduce immediate tensions surrounding the Strait of Hormuz. However, Iran’s insistence on not returning to pre-28 February conditions suggests that Tehran is unlikely to abandon demands for imposing tolls or expanded oversight over tanker movements through the strait.

Should Iran succeed in institutionalizing such practices, it could establish a precedent for similar actions at other strategic chokepoints, particularly the Bab al-Mandeb, where Iran-aligned Houthis maintain operational presence.

Such a development would significantly increase risks to global maritime trade because Bab al-Mandeb also constitutes a critical artery for international energy shipments linking the Gulf of Aden with the Red Sea and the Suez Canal.

The crisis has additionally increased concerns among Gulf states regarding Iran’s effective leverage over the primary maritime route through which much of their crude oil exports transit. Given Iran’s strained relations with several regional countries, Gulf states increasingly view Tehran’s ability to influence tanker passage as a major long-term strategic vulnerability.

Pipeline Alternatives and Infrastructure Vulnerability

In response, Gulf countries have intensified discussions regarding alternative oil transportation infrastructure, particularly pipelines capable of bypassing Hormuz entirely.

Saudi Arabia and the UAE already possess pipeline infrastructure bypassing the Strait of Hormuz, which has allowed both to maintain a degree of export continuity during the crisis, but they are planning to expand it further. Observing Saudi Arabia’s and the UAE’s relative resilience, other Gulf states are increasingly considering similar projects.

However, pipelines have major limitations. They cannot transport oil volumes comparable to shipping routes, while many proposed pipelines would pass through unstable regions such as Iraq and Syria, making them vulnerable to attacks and regional tensions. Moreover, such alternatives are also expensive.

Consequently, while pipelines may reduce dependence on Hormuz, they are unlikely to fully replace the strategic importance of maritime transit through the strait.

Strategic Lessons from the Hormuz Crisis

The Hormuz crisis demonstrates that countries can no longer assume strategic waterways will remain secure during geopolitical escalation. Countries are therefore likely to increase investment in maritime surveillance, naval response capabilities, strategic petroleum reserves, and alternative logistical infrastructure to reduce vulnerability to future disruptions. The crisis also highlights the need to diversify energy sources, transport corridors, and critical mineral supply chains to reduce dependence on concentrated routes and commodities.

Conclusion

The current Hormuz crisis demonstrates that the weaponization of international waterways is no longer merely a regional security issue but a major threat to global economic stability. Iran’s ability to disrupt global energy markets despite limited naval capabilities has exposed the vulnerability of the international trading system to maritime coercion. The crisis also highlights that even partial disruptions to strategic chokepoints such as the Strait of Hormuz and Bab al-Mandeb can generate severe economic, commercial, and geopolitical consequences far beyond the immediate conflict zone.